Living in Katy, Texas, you don’t just have a roof—you have a first line of defense against hail, wind, and heavy Gulf Coast storms. When something happens to that roof, your insurance policy becomes just as important as your shingles.

That’s when you run into the big question:

Does your policy cover your roof at Actual Cash Value (ACV) or Replacement Cost (RCV)?

Understanding actual cash value vs replacement cost roof in Katy, Texas can easily mean the difference between a manageable out-of-pocket cost and a nasty financial surprise.

What Is Actual Cash Value (ACV) for Your Roof?

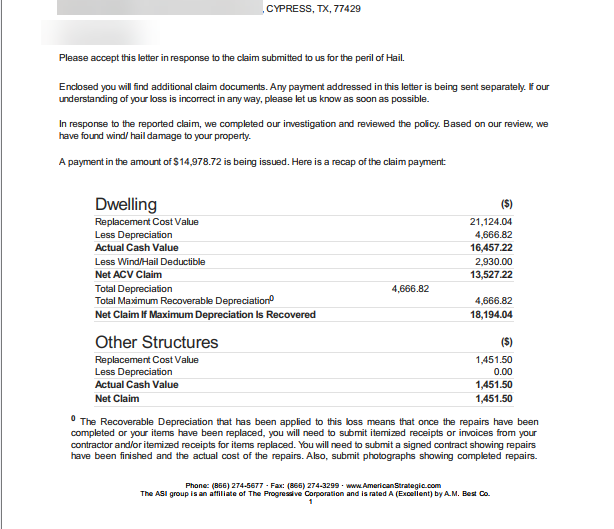

Actual Cash Value (ACV) means your insurance company pays what your roof is worth today — after factoring in age, wear, and depreciation.

Think of ACV like this:

New roof price – depreciation = ACV payout

Example of an ACV roof payout in Katy, TX

Cost to replace roof today: $20,000

Your roof is 10–12 years old

Insurance depreciates it by, say, 50%

Depreciation: $10,000

Deductible: $3,000

ACV payment:

$20,000 – $10,000 (depreciation) – $3,000 (deductible) = $7,000

You’d be short $13,000 if you wanted a full replacement.

That’s how ACV works: it helps, but it usually doesn’t fully pay for a brand-new roof.

What Is Replacement Cost (RCV) for Your Roof?

Replacement Cost Value (RCV) means your policy is designed to pay what it actually costs to replace your roof with a similar kind and quality at today’s prices (minus your deductible).

With RCV, the insurance company typically pays in two steps:

Initial ACV payment – They pay the actual cash value up front.

Recoverable depreciation – Once the roof is replaced and proof of completion is provided, they release the remaining amount (the “depreciation”).

Using the same example:

Replacement cost: $20,000

Depreciation: $10,000

Deductible: $3,000

You still pay your $3,000 deductible, but instead of keeping that $10,000 depreciation, the insurance company pays it back after the work is done.

So instead of getting $7,000 like with ACV and being stuck, you end up with $17,000 total from insurance, and you pay your $3,000 deductible. That usually makes a full roof replacement possible.

Actual Cash Value vs Replacement Cost Roof in Katy, Texas: Key Differences

Here’s a simple breakdown of ACV vs RCV roof policies:

| Feature | ACV (Actual Cash Value) | RCV (Replacement Cost Value) |

|---|---|---|

| How payout is calculated | Replacement cost minus depreciation | Replacement cost (no depreciation withheld long term) |

| Upfront check | Lower | Higher in total (ACV + depreciation later) |

| Out-of-pocket costs for homeowner | Typically higher | Typically lower (besides deductible) |

| Older roofs | Much less coverage | More protection if still eligible |

| Monthly premiums | Usually cheaper | Usually more expensive |

| Best for | Investors, landlords accepting more risk | Homeowners wanting to fully protect their home |

In a storm-prone area like Katy, Texas, that difference is huge when you’re deciding how to protect your home and budget.

How Roof Insurance Claims Typically Work in Texas

When you file a roof insurance claim in Katy, TX after hail or wind damage, the process often looks like this:

Inspection & claim filed

You or your roofer notice damage (missing shingles, hail bruising, lifted shingles, leaks, etc.) and file a claim.Adjuster inspection

The insurance company sends an adjuster to inspect your roof. A good local roofing contractor can meet them there to point out storm-related damage.Initial estimate & ACV payment

Insurance creates an estimate for the damage.If you have ACV, your payment reflects depreciation + deductible.

If you have RCV, the first check is usually ACV, with recoverable depreciation to come later.

Roof replacement or repair

You hire a licensed roofing company (like All Out Roofing in Katy) to complete the work per the approved scope. Sometimes your roofer will help with supplements if items were missed.Final invoice & recoverable depreciation (RCV only)

If your policy is RCV, once the work is complete and documented, the remaining depreciation is released and paid to you or your roofer.

Pros and Cons of ACV vs Replacement Cost Roof Coverage

Pros of ACV Roof Coverage

Lower premiums – Monthly insurance costs are usually less.

Works for older roofs that may not qualify for RCV in some policies.

Can be okay if you’re prepared to pay out-of-pocket or planning a full remodel anyway.

Cons of ACV Roof Coverage

Big out-of-pocket hit when you actually need a new roof.

Heavier depreciation on older roofs in Katy’s heat and storms.

Can make full replacement unaffordable without savings or financing.

Pros of RCV Roof Coverage

Better protection for your largest asset – your home.

More likely to cover a full roof replacement after a covered storm event.

Great fit for primary residences in high-storm regions like Katy, Fulshear, and the Greater Houston Area.

Cons of RCV Roof Coverage

Higher premiums than ACV.

Must actually repair or replace the roof to receive the full payment (including depreciation).

Some policies may adjust coverage as your roof ages (important to review your declarations page).

How to Tell If You Have ACV or Replacement Cost on Your Roof Policy

Most homeowners in Katy never look at this until after a storm — when it’s too late to change it. Here’s how to check now:

Grab your policy & declarations page

Look for terms such as:“Loss Settlement – Actual Cash Value”

“Replacement Cost Coverage for Dwelling Roof”

“Wind/Hail – ACV Only” (this one is big — some policies are RCV overall but ACV for the roof).

Look for roof-specific endorsements

Sometimes your policy says you have replacement cost on the home but ACV specifically on the roof. That’s a common money-saver in Texas — and a common shock after a storm.Call your agent

Ask directly:“Is my roof covered at actual cash value or replacement cost for wind and hail?”

Document the answer

Add a note to your policy: “As of [date], agent confirmed: roof is covered at [ACV/RCV].” It’s not official policy language, but it’s a good reminder for you.

What Makes Sense in Katy, Texas: ACV or Replacement Cost?

Because Katy sees:

Hail storms

Heavy rain and wind

Occasional hurricanes/tropical systems

Extreme sun and heat that age shingles faster

…your roof isn’t a “maybe one day” repair. It’s a guaranteed future expense.

Many homeowners in Katy, Cinco Ranch, Firethorne, Elyson, and nearby neighborhoods find that RCV roof coverage gives them better peace of mind, even with a slightly higher premium.

However, if:

The home is a rental or investment property

The roof is already older and near the end of its life

You keep strong reserves in savings

…then ACV coverage may make sense for your situation, as long as you understand you’re accepting more risk if a storm hits.

Common Mistakes Homeowners Make With Roof Insurance in Katy

Assuming they have replacement cost when they don’t

They file a claim expecting a full roof but get an ACV check that won’t cover the job.Waiting too long after a storm

Insurance companies often have deadlines to file claims after an event. Waiting can cause denial.Ignoring small leaks and missing shingles

These can become interior damage, decking rot, and even mold—issues insurance may say are “maintenance,” not storm-related.Choosing the cheapest roofer

A low bid that ignores code, ventilation, or quality materials can cost you in the long run. And if the contractor can’t work with your insurance estimate, you may end up paying more out of pocket than necessary.

How All Out Roofing Helps With ACV & RCV Roof Claims in Katy, Texas

At All Out Roofing, we work with Katy-area homeowners every day who are trying to figure out exactly this question:

“What does my policy actually cover, and what will my new roof really cost?”

Here’s how we help:

✅ Free roof inspections after wind or hail storms in Katy, Fulshear, Richmond, and the Greater Houston area

✅ Photo and video documentation of storm damage to support your claim

✅ Clear explanations of the difference between actual cash value vs replacement cost roof coverage in plain English

✅ Help reviewing the insurance estimate so you understand what’s included (and what might be missing)

✅ High-quality shingle and roofing system options that meet Texas codes and manufacturer specs

✅ Honest guidance on whether repair or replacement makes the most sense for your situation

We’re not an insurance company and we don’t give legal advice, but we do help homeowners feel confident when they talk to their agent or adjuster.

Final Thoughts: Know Your Coverage Before the Next Storm

If there’s one takeaway, it’s this:

Don’t wait until after a storm to find out if you have ACV or RCV coverage on your roof.

Understanding actual cash value vs replacement cost roof in Katy, Texas today gives you time to:

Adjust your coverage if needed

Budget for a deductible

Choose a trusted, local roofing company to call when something happens

Need Help With a Roof in Katy, TX?

If you’re unsure what your policy will actually pay — or you suspect you already have storm damage — we’d be happy to take a look.

All Out Roofing – Katy, Texas

📞 281-769-3738

🌐 alloutroofs.com

Schedule a free roof inspection today and let us help you make sense of your ACV vs RCV roof coverage before the next Texas storm rolls through.